Menu

-

News

Genetically edited crops to begin trials in England

Hay fires are becoming more frequent in Kazakhstan

Weather forecasters will continue to forecast difficulties in harvesting

Sugar producer asks to raise investment subsidies

The best sheep were chosen at a competition in the Turkestan region

Today, a complete ban on wheat imports came into force

China needs grain supplies from Kazakhstan on a permanent basis

Russia may ban the export of original seeds

Kyrgyzstan has quintupled imports of cattle from Kazakhstan

Farmers developing villages deserve respect

-

Blogs

Will Uzbekistan stop buying Kazakh meat?

Russia needs Kazakh beef

What does the state and farmers need?

ACROS 595 Plus: When you need more

Export of Kazakh barley under threat

Do Kazakh farmers need innovation?

Is there a need for an agricultural census in Kazakhstan?

In 30 years, has the agro-industrial complex only regained the performance of the 1990s?

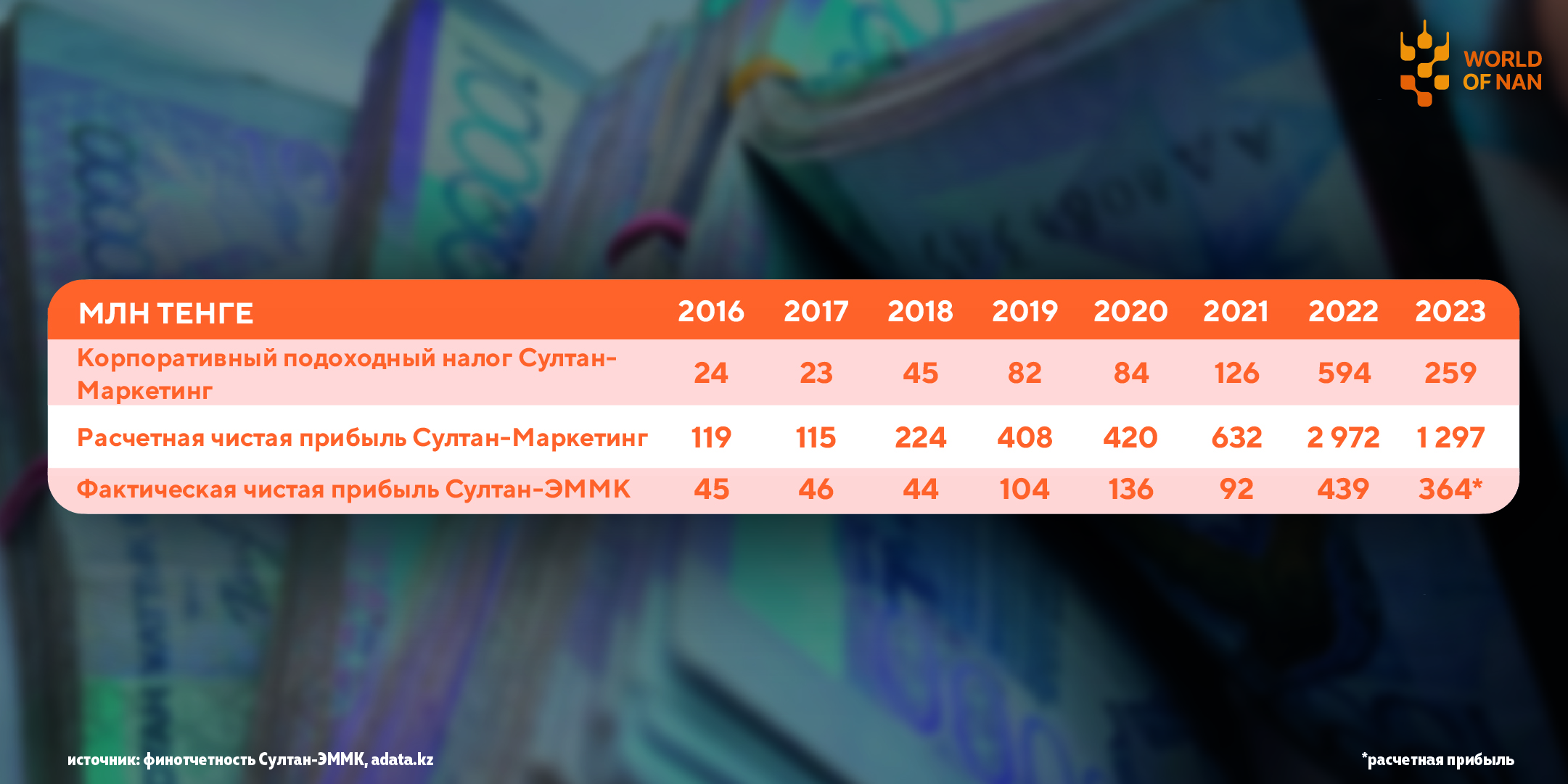

How much of the government money passes through NASEC?

Who will win in the war between processors and farmers?

-

Media library

The Earth gravity

Dosym Satpayev's film "Nomads of the Dead Steppe"

What will the dairy farm of the future look like?

DIGITAL MTS BY EURASIA CROP CARE

Farmers tested agricultural machinery at the KazAgroExpert exhibition site

International agricultural exhibition

III EAEU Conference in the capital of Kazakhstan

AgriTek/FarmTek Astana2020

- Posters

-

Video

Farmers tested agricultural machinery at the Kaz...

DIGITAL MTS BY EURASIA CROP CARE

What will the dairy farm of the future look like?

STEPAN TEN: "THE BIGGEST CHALLENGE IN THE DAIRY ...

Nature is so clever that all solutions can be fo...

XIII Dairy Olympics

Bumblebees boost harvests

A wonder shovel for farmers by Stenon

The geography of exports is expanding. What will...

Yerlan Nurtazin: "the state does not support the...

Sowing campaign in Shymkent has started

How can a company influence a farmer's harvest?

Kintal Islamov: "Any restrictions make our life ...

Weather forecasters have announced sowing dates ...

Blitz survey: how have the anti-Russian sanction...

-

Investmets

What plans does CLAAS have in Kazakhstan?

Greenhouse based on Israeli technology is planned to be opened in the south

Sugar factory is looking for an investor

Qatar is interested in Kazakhstan's agro-industrial complex

Industries of Kazakhstan

China and Turkey are investing in agricultural projects in Kazakhstan

Plants of Kazakhstan

Natural Resources of Kazakhstan

Belgium to expand contacts with Kazakh flax exporters

A Kazakh scientist has developed a method of obtaining fertilizer from rice husks

Обсуждение